Quick Facts

- Market Context: Total U.S. home equity for homeowners with a mortgage reached a record $17.6 trillion in the second quarter of 2024.

- Investment Power: The average mortgage holder currently possesses approximately $303,000 in equity, representing a significant untapped reserve.

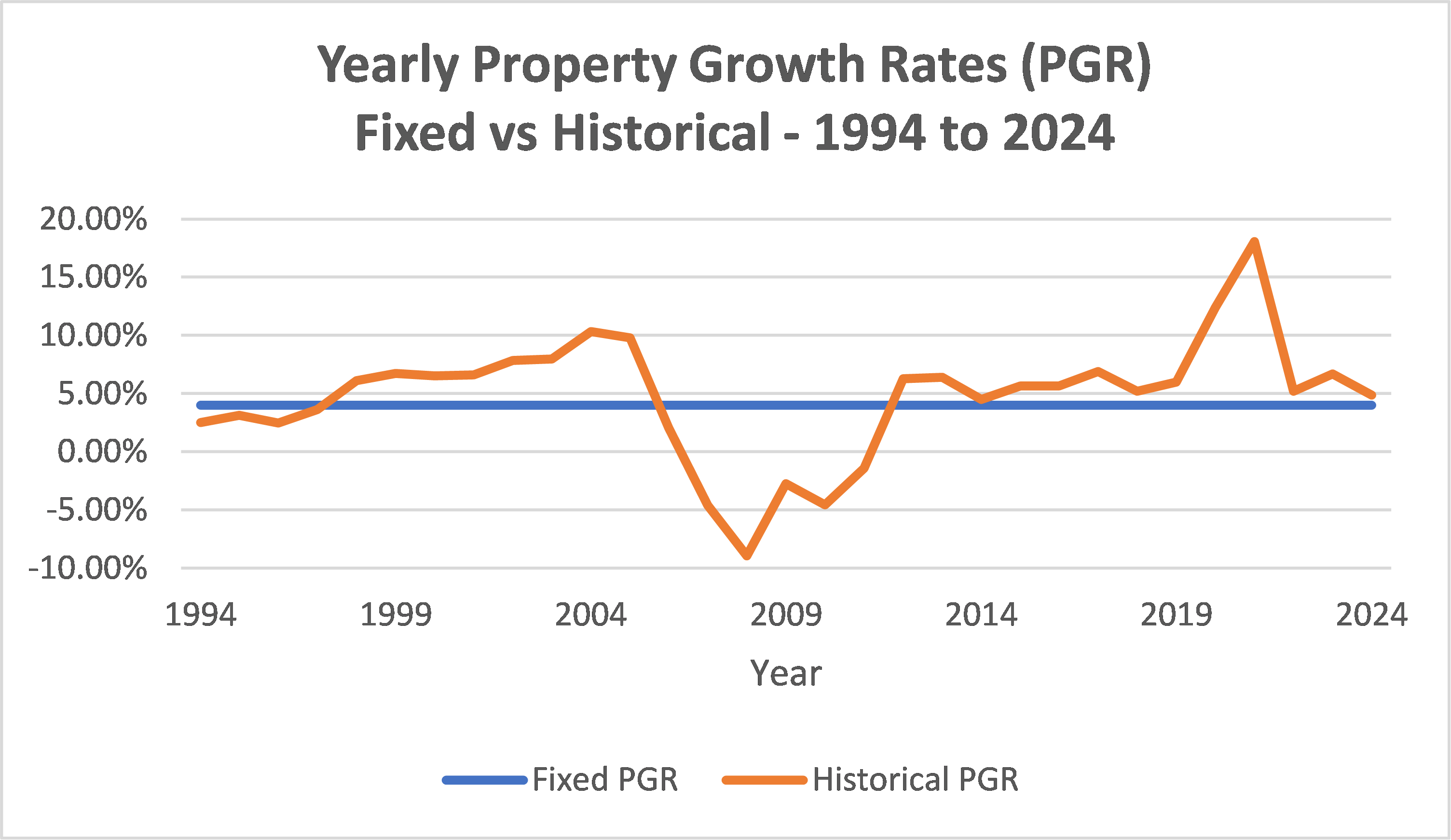

- Strategic Floor: Historical data shows the 30-year U.S. housing compound annual growth rate holds steady at 4.7%, providing a stable foundation for a home equity retirement asset.

- Age Requirement: Homeowners must be at least 62 years old to qualify for a Home Equity Conversion Mortgage (HEM), a primary tool for equity extraction.

- The 80% Rule: Most traditional lenders cap usable home equity at an 80% loan-to-value ratio to ensure a safety buffer for the property owner.

- Privacy and Protection: HUD-insured HECMs include non-recourse protections, ensuring heirs are not held liable if the loan balance exceeds the home value at the time of sale.

As we enter 2026, the paradigm has shifted: home equity is no longer just stored value but a core home equity retirement asset. With Americans holding record levels of housing wealth, sophisticated retirees are moving beyond traditional 401(k) withdrawals and integrating housing wealth into their primary portfolio strategies to combat sequence of returns risk.

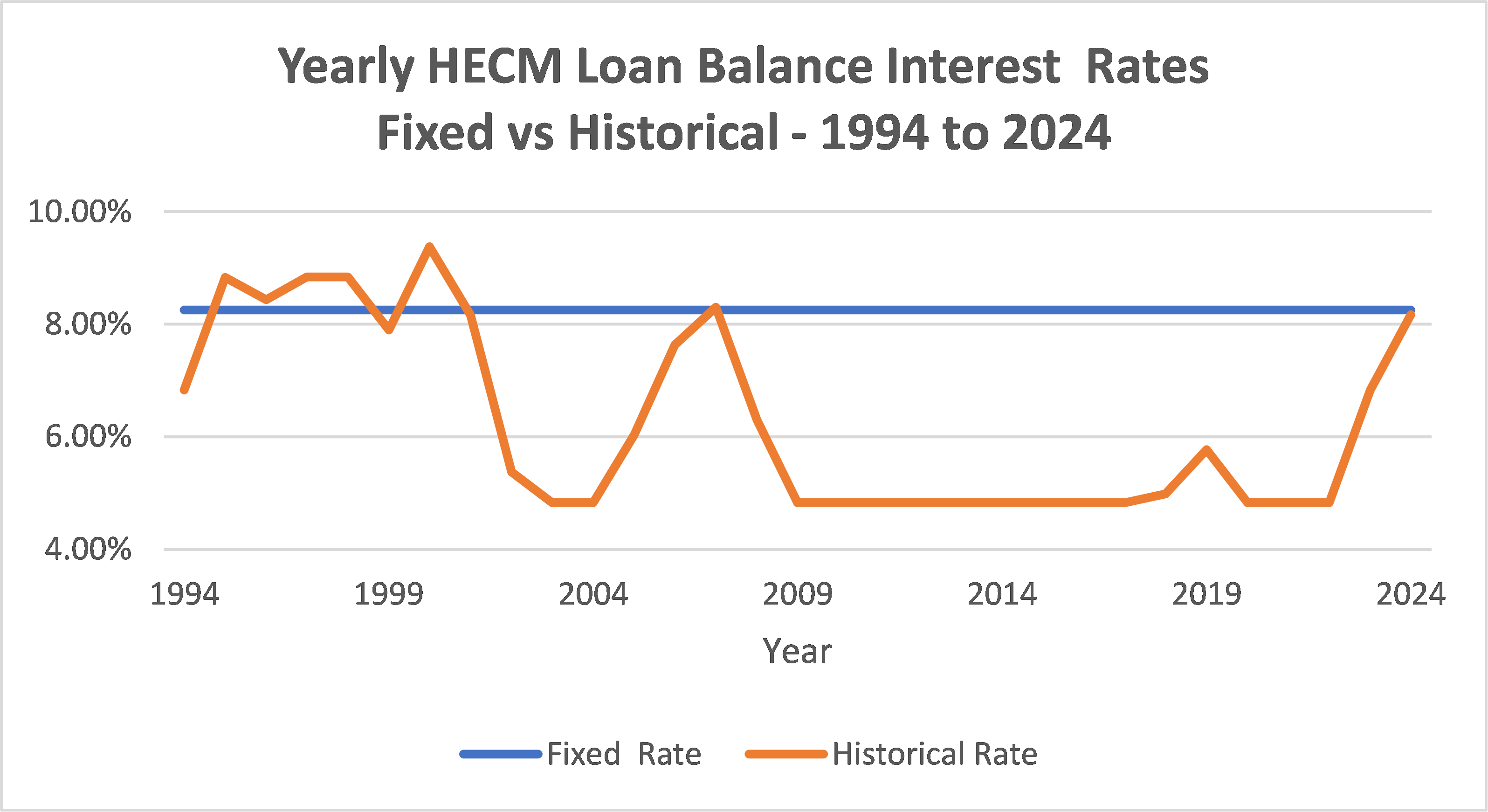

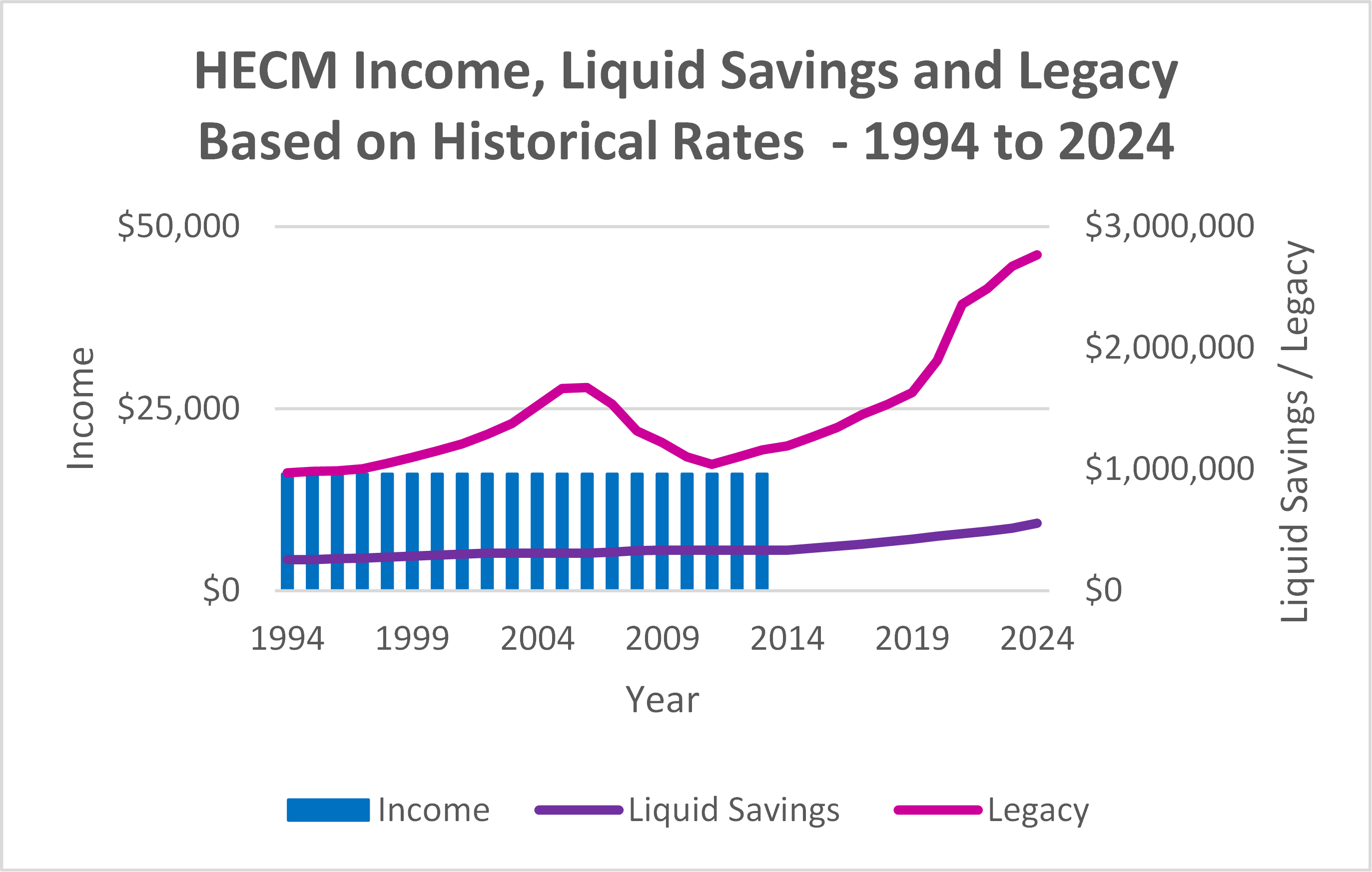

Utilizing home equity as a retirement asset involves treating property value as a managed investment class rather than just a place to live. Strategies like Home Equity Conversion Mortgages allow retirees to access non-taxable cash flow while maintaining ownership of the home. By stress-testing home equity against historical housing price indices and interest rate fluctuations, homeowners can better manage liquid savings for long-term care and legacy objectives.

Section 1: The 'Usable Equity' Audit

To manage property wealth effectively, you must first distinguish between total market value and investable power. For the typical U.S. homeowner, home equity accounts for a median of 45% of total household net worth, making it the largest single financial asset in many portfolios. However, being equity-rich cash-poor is a common trap where homeowners have high net worth on paper but struggle with monthly liquidity.

The first step in home equity asset management retirement is performing a usable equity audit. While your home may be valued at $600,000, lenders generally adhere to an 80% loan-to-value ratio. This means your maximum borrowing power, including any existing mortgage, is $480,000. Subtracting your remaining mortgage balance from this figure reveals your actual liquid power.

By late 2024, approximately 48 million U.S. homeowners held a collective $11.2 trillion in 'tappable' equity, allowing them to access an average of $207,000 each while maintaining a 20% equity stake. Understanding these numbers is essential for net worth optimization. High-net-worth individuals often use this calculation to decide whether to downsize or utilize a specialized loan structure to remain in place while freeing up capital.

Rule of Thumb: The 80% LTV Rule To calculate your usable equity, multiply your home's current market value by 0.80. Subtract any outstanding mortgage balances or liens. The remaining number represents the capital you can theoretically deploy into your wider retirement plan without selling the asset.

This audit helps bridge the gap for home equity asset management for equity rich retirees who may have millions in real estate but insufficient distributions from their retirement accounts. By identifying this capital early, you can integrate it into a broader financial framework that accounts for inflation and rising healthcare costs.

Section 2: HECM vs. Trad Loans: The Strategy Selection Matrix

Once you identify your usable equity, the focus shifts to the mechanism of extraction. Many retirees reflexively look toward a standard Home Equity Line of Credit (HELOC), but for those over age 62, a HECM retirement strategy often provides superior long-term results.

A standard HELOC typically requires monthly interest payments and has a fixed "draw period" after which the loan must be repaid or refinanced. Conversely, a HECM is a reverse mortgage that requires no monthly principal or interest payments as long as the homeowner lives in the house, pays property taxes, and maintains the residence.

| Feature | Traditional HELOC | HECM (Reverse Mortgage) |

|---|---|---|

| Monthly Payments | Required (Interest or P&I) | Optional (No monthly P&I required) |

| Credit Line Growth | Line is fixed or can be frozen | Grows over time regardless of home value |

| Repayment Requirement | Monthly or at end of term | When last borrower leaves home |

| Credit/Income Check | Stringent requirements | Moderate (Focus on taxes/insurance) |

| Asset Safety | Can be cancelled by lender | Guaranteed by FHA regulatory backing |

The defining feature of a HECM is the growing line of credit. Unlike a traditional bank loan where the limit stays static, the unused portion of a HECM line of credit increases at the same rate as the interest on the loan. This means your available liquidity grows even if the market experiences a downturn. Deciding between home equity loans and HECMs for retirement depends heavily on your cash flow needs and whether you prioritize debt elimination or future liquidity.

When retirees are using HECM as market volatility protection for retirees, they are essentially creating an emergency fund that expands the longer it stays untouched. This provides a level of longevity risk mitigation that a standard loan simply cannot match. If the Housing Price Index stalls, the HECM borrower is protected by federal insurance, ensuring that their available credit remains intact.

Section 3: The Volatility Buffer: Hedging Your 401(k)

The most sophisticated use of housing wealth is implementing a home equity market volatility protection strategy. The biggest threat to a retirement portfolio is sequence of returns risk. This occurs when a retiree is forced to sell stocks or mutual funds at a loss during a market crash to meet their living expenses.

When you extract cash from a depressed 401(k), you lock in those losses and permanently reduce the portfolio's ability to recover. Integrating home equity into retirement portfolio assets creates a "standby" source of funds. During a year when the stock market is down 10% or 20%, instead of selling shares, you can draw from a home equity line.

This allows your equity investments the necessary time to rebound. This buffer approach effectively creates a diversified asset management plan where your home acts as the "bond" or "cash" portion of your portfolio. By managing the timing of your distributions, you can significantly extend the life of your total liquid assets.

For example, a retiree with a $1 million portfolio and a $300,000 HECM line of credit has much higher survival probability for their funds than one who relies solely on the portfolio. Integrating these strategies helps stabilize the total net worth and reduces the emotional stress of watching market fluctuations. It turns your home from a dormant liability that costs money in taxes and maintenance into an active financial insurance policy.

Section 4: Tax Optimization and Legacy Planning

One of the largest advantages of utilizing home equity is the tax treatment. Funds received from a HECM or a home equity loan are considered loan proceeds, not income. This results in non-taxable cash flow.

For retirees facing heavy tax burdens from Required Minimum Distributions (RMDs), using home equity can be a strategic move. By taking a portion of your needed annual income from your home equity retirement asset tax advantages instead of your traditional IRA, you can keep your taxable income in a lower bracket. This can also help reduce the impact of the "tax torpedo" where higher income leads to increased taxes on Social Security benefits.

Furthermore, integrating home equity strategies with Qualified Longevity Annuity Contracts helps mitigate longevity risk and optimize net worth. This combination allows retirees to defer required minimum distributions while securing guaranteed lifetime income for their later years. Using a home equity line of credit to supplement cash flow during market downturns allows other retirement assets to remain untouched and recover, creating a more resilient financial plan for aging in place.

Rule of Thumb: Managing Heir Intentions Under HUD regulations, heirs are protected by the 95% rule. If the loan balance is higher than the home's value when the borrower passes, heirs can purchase the home for 95% of its current appraised value, or simply let the lender sell the property with no personal liability for the deficit.

When managing home equity legacy impact for heirs, it is important to realize that spending down equity does not necessarily mean leaving nothing behind. In fact, by using home equity to preserve your 401(k), you may actually leave a larger, more liquid inheritance (like a stepped-up basis in a brokerage account) than if you had exhausted your cash and left only a house that must be sold anyway.

Proper estate planning should always include fiduciary financial advice to ensure that the use of home equity aligns with your long-term goals for both your lifestyle and your beneficiaries.

FAQ

Is home equity considered a retirement asset?

Yes, home equity is increasingly viewed as a core retirement asset. Because it represents a significant portion of household net worth and can be converted into non-taxable cash flow through specific financial instruments, it acts as a strategic reserve that can supplement traditional retirement accounts.

How can I use home equity to fund my retirement?

Retirees typically fund their lifestyle through several methods: downsizing to a less expensive home to pocket the difference, taking out a Home Equity Line of Credit (HELOC), or setting up a Home Equity Conversion Mortgage (HECM). These tools allow you to tap into property value to cover daily expenses, healthcare costs, or to serve as a buffer during market downturns.

What are the risks of using home equity as a retirement asset?

The primary risks include the accumulation of interest which reduces the remaining equity in the home, the cost of upfront fees associated with specialized loans, and the requirement to remain in the home as a primary residence. If you need to move to assisted living unexpectedly, the loan may become due, requiring the sale of the property.

How does home equity fit into a retirement plan?

Home equity fits into a plan as a "third tier" of funding. The first tier is usually guaranteed income (Social Security/Pensions), the second is personal savings (401k/IRA), and the third is housing wealth. It can be used strategically to manage tax brackets or as a contingency fund for long-term care needs that aren't covered by traditional insurance.

Can I get a home equity loan while retired?

Yes, it is possible to get a home equity loan while retired, though it can be more challenging with traditional lenders who focus heavily on active income. However, the HECM was specifically designed for retirees; it uses the home's value and the borrower's age as the primary qualifying factors rather than current monthly salary.

What are the tax implications of using home equity for retirement?

Generally, the funds you receive from home equity loans or HECMs are considered non-taxable cash flow because they are loan proceeds rather than earned income. This can help retirees stay in lower tax brackets and avoid higher surcharges on Medicare premiums that are triggered by high levels of taxable income.