Quick Facts

- 20-Year ROI: An initial $1,000 investment would be worth approximately $2,700 today.

- Annualized Return: UPS has delivered a 5.2% annualized total return over two decades.

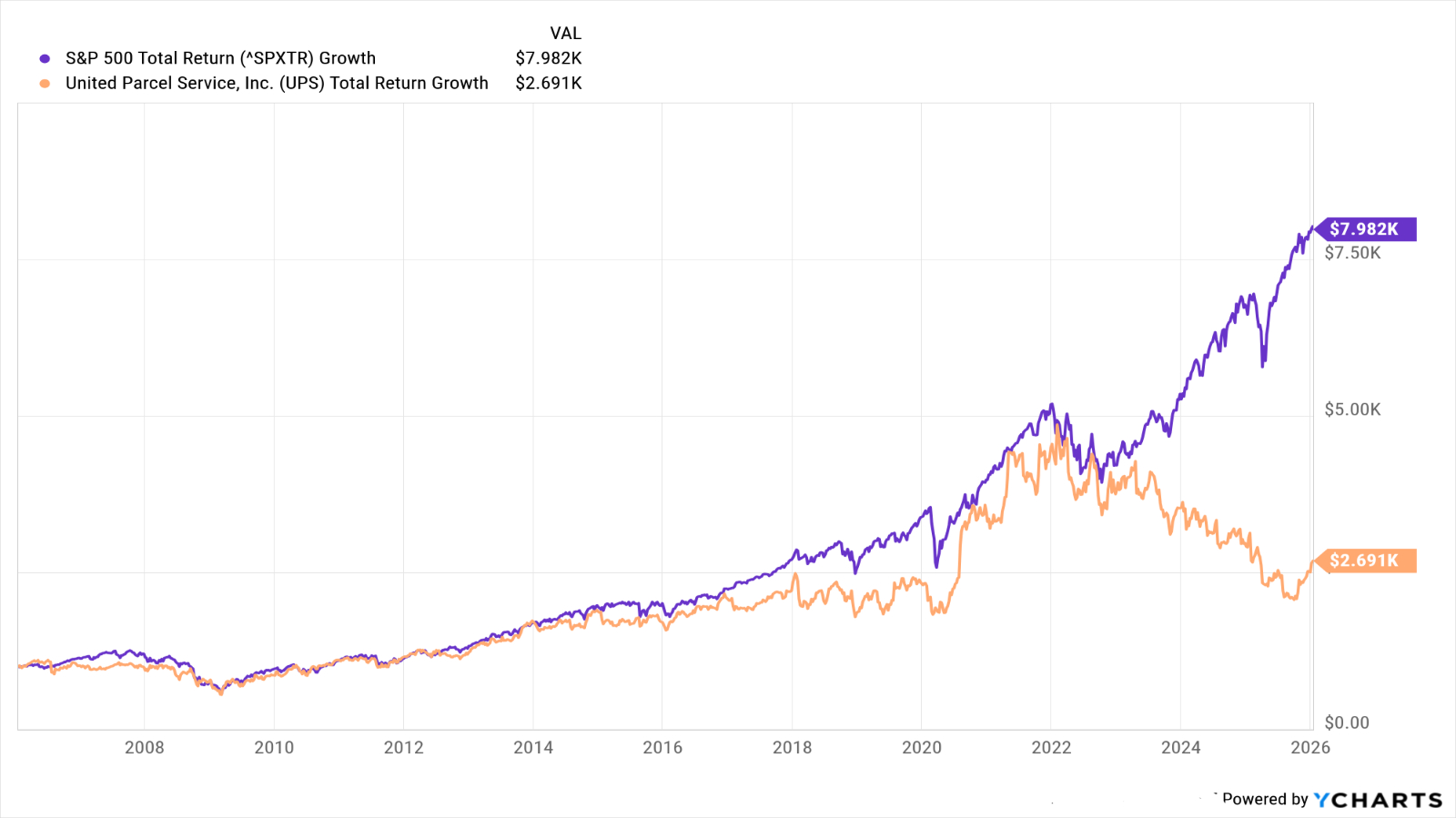

- Market Comparison: This performance significantly trails the S&P 500, which turned $1,000 into nearly $8,000.

- Dividend Growth: The company has increased payouts for 17 consecutive years with an 8% compound growth rate.

- 2026 Financial Targets: Management is guiding for $89.7 billion in revenue and a 9.6% adjusted operating margin.

- Capital Allocation: Approximately $1 billion is earmarked for stock buybacks in the 2026 fiscal year.

- Strategic Pivot: The company is focused on high-margin segments through a deliberate decoupling from Amazon.

If you had invested $1,000 in UPS stock 20 years ago, your investment would be worth approximately $2,700 today when accounting for price appreciation and reinvested dividends. While this represents a steady gain, UPS stock returns have largely underperformed the broader market, which would have grown an equivalent investment into nearly $8,000 over the same period.

Historical Performance: UPS vs. the S&P 500

When evaluating the long-term viability of a portfolio staple like United Parcel Service (UPS), perspective is everything. As a long-term investor, looking at UPS stock returns requires a deep dive into the mechanics of the logistics sector. UPS functions as an industrial bellwether, a company whose health often mirrors the broader economy. However, being an industrial bellwether comes with a specific set of challenges, most notably the requirement of an asset-heavy business model. Unlike the software giants that dominate the modern S&P 500, UPS must maintain a massive fleet of over 500 planes, thousands of vehicles, and a globally integrated sortation network.

The historical data highlights a clear divergence in performance. A $1,000 investment made two decades ago would have yielded a total return of roughly 170%, translating to a 5.2% annualized return. In contrast, the S&P 500 delivered a 10.9% annualized return during that same window. This gap illustrates the struggle of capital-intensive businesses to keep pace with the high-margin, scalable growth seen in the technology and consumer discretionary sectors. Even if we look at the ROI of 1000 dollar investment in UPS over 20 years, the conclusion remains that while UPS has been a wealth builder, it has not been a market leader.

Looking back even further to the company's roots as a public entity, the numbers are equally sobering for early adopters. A $1,000 investment in UPS stock made at its initial public offering in November 1999 would be worth approximately $2,358 as of May 2026. This reflects a compound annual growth rate of about 4.6% over more than a quarter-century. This slow and steady trajectory is a hallmark of the logistics sector, where profit growth is often capped by labor costs and fuel volatility.

The recent decade has seen more pronounced fluctuations. For instance, a $1,000 historical investment in UPS stock made 10 years prior to March 2026 would be worth roughly $1,436, reflecting a total return of 43.6%. When comparing UPS stock performance vs S&P 500 benchmarks, it is clear that the logistics giant has faced headwinds that the broader market has managed to sidestep, specifically the post-pandemic normalization of shipping volumes and rising domestic labor expenses.

The Income Play: UPS Dividend Yield History

For many investors, the primary draw to UPS is not explosive capital appreciation but consistent income. Analyzing the UPS dividend yield history reveals a company deeply committed to returning value to shareholders, even when the underlying stock price remains stagnant. UPS has maintained a strong track record for income-focused portfolios, raising its dividend annually for 17 years. This is part of a larger 26-year streak of either maintaining or increasing its payout.

Over the last two decades, the UPS dividend growth rate last 20 years has surpassed 8% on a compound annual basis. This aggressive growth in the payout has helped offset some of the sluggishness in the stock price. For a value investing practitioner, the high dividend yield often serves as a "floor" for the stock's valuation, attracting buyers whenever the yield reaches historically high levels.

However, there is a nuance to the current capital allocation strategy that investors must monitor. By early 2026, the company’s payout ratio has occasionally exceeded 100% of its GAAP earnings. While this is often a red flag for a potential dividend cut, management has signaled that this is a temporary byproduct of their massive internal restructuring and the "Better Volume" pivot. They are betting that future earnings growth will bring the payout ratio back down to a more sustainable 60-70% range. For those seeking total shareholder return, the stability of these payouts has been the saving grace that prevents the 20-year performance from looking even more unfavorable against the S&P 500.

The 2026 Inflection Point: Strategy & Buybacks

The narrative for UPS in 2026 is centered on what management calls an inflection point in profitability. After several years of battling declining parcel delivery demand and the high costs associated with a new labor contract, the company is finally seeing its strategic decoupling from Amazon bear fruit. Historically, Amazon was one of the largest customers for UPS, but the relationship came with thin margins and high operational complexity. By intentionally reducing its reliance on Amazon, UPS is pursuing revenue mix optimization, focusing instead on high-margin sectors like healthcare logistics and small-to-medium-sized businesses (SMBs).

This shift is a key component of the impact of Amazon decoupling on UPS stock growth. Management is targeting a 2026 revenue goal of $89.7 billion with an adjusted operating margin of 9.6%. To get there, the company is executing a massive cost-savings initiative aimed at cutting $3.5 billion in expenses. This includes the difficult task of eliminating approximately 30,000 management and support roles to lean out the corporate structure.

From an investor's perspective, the UPS stock buyback program 2026 details are a sign of confidence. The company plans to spend approximately $1 billion on stock buybacks this year. This signifies that management believes the stock is currently undervalued relative to the cash-flow generation they expect from their improved network density and labor productivity gains. When companies buy back stock at the same time they are achieving higher-margin volume, it typically leads to an acceleration in earnings per share (EPS).

Valuation and Risks: Investor Outlook

Current UPS analyst recommendations present a cautiously optimistic view of the stock as it nears its 2026 goals. The bull case for the stock rests on the idea that the "Earnings Valley" of 2023-2025 is now in the rearview mirror. Investors are looking at a free cash flow (FCF) yield that has become quite attractive. While the asset-heavy nature of the business requires constant reinvestment, the move toward automation in its sortation hubs is expected to drive long-term margin expansion.

Setting realistic UPS analyst price targets for 2026 requires balancing these operational improvements against macro headwinds. The primary risk remains e-commerce normalization. During the pandemic, shipping volumes surged to unsustainable levels, and the industry has spent the last three years adjusting to the comedown. If global consumer spending softens further, even a more efficient UPS will find it difficult to hit its $89.7 billion revenue target.

Furthermore, valuation multiples for the logistics sector have remained compressed compared to high-growth tech sectors. UPS is often valued on its forward P/E and EV/EBITDA ratios, which currently suggest the market is still in a "show me" mode. Investors are waiting to see if that 9.6% operating margin is a one-time peak or a sustainable new baseline. For those focused on a risk-aware strategy, UPS represents a defensive play with a high income component, provided the investor can stomach the slower growth profile inherent in the domestic package delivery industry.

FAQ

How much would $1000 invested in UPS ten years ago be worth today?

A $1,000 investment in UPS stock made ten years ago would be worth approximately $1,436 today. This indicates a total return of 43.6% over the decade, which falls short of the gains seen in the broader market indices during the same period.

What is the total return of UPS stock over the last 5 years?

The last five years have been particularly volatile for UPS. Due to the rapid spike in volume during the pandemic followed by a sharp normalization and rising labor costs, a $1,000 investment five years ago would be worth roughly $598 today, representing a significant negative impact on recent portfolios when compared to previous decades.

Does UPS stock pay a high dividend?

Yes, UPS is well-known for its commitment to income investors. It currently offers a competitive dividend yield and has maintained a track record of increasing its annual payout for 17 consecutive years, making it a common choice for investors seeking a value investing strategy.

How has UPS stock performed compared to the S&P 500?

Over almost any long-term timeframe (10, 20, or 25 years), UPS has underperformed the S&P 500. For instance, over 20 years, UPS delivered an annualized return of 5.2% compared to 10.9% for the S&P 500, largely because the logistics sector is more capital-intensive and sensitive to labor costs than the tech-heavy benchmark.

Is UPS stock a good buy for dividend growth?

UPS remains a strong candidate for dividend growth, having increased its dividend at a compound annual rate of over 8% over the last 20 years. While its current payout ratio is high, management's 2026 strategic plan aims to grow margins and revenue, which would provide better coverage for future dividend increases.