Quick Facts

- The Core Benefit: Qualified Opportunity Funds allow for the indefinite deferral of current capital gains taxes and the complete elimination of taxes on future appreciation.

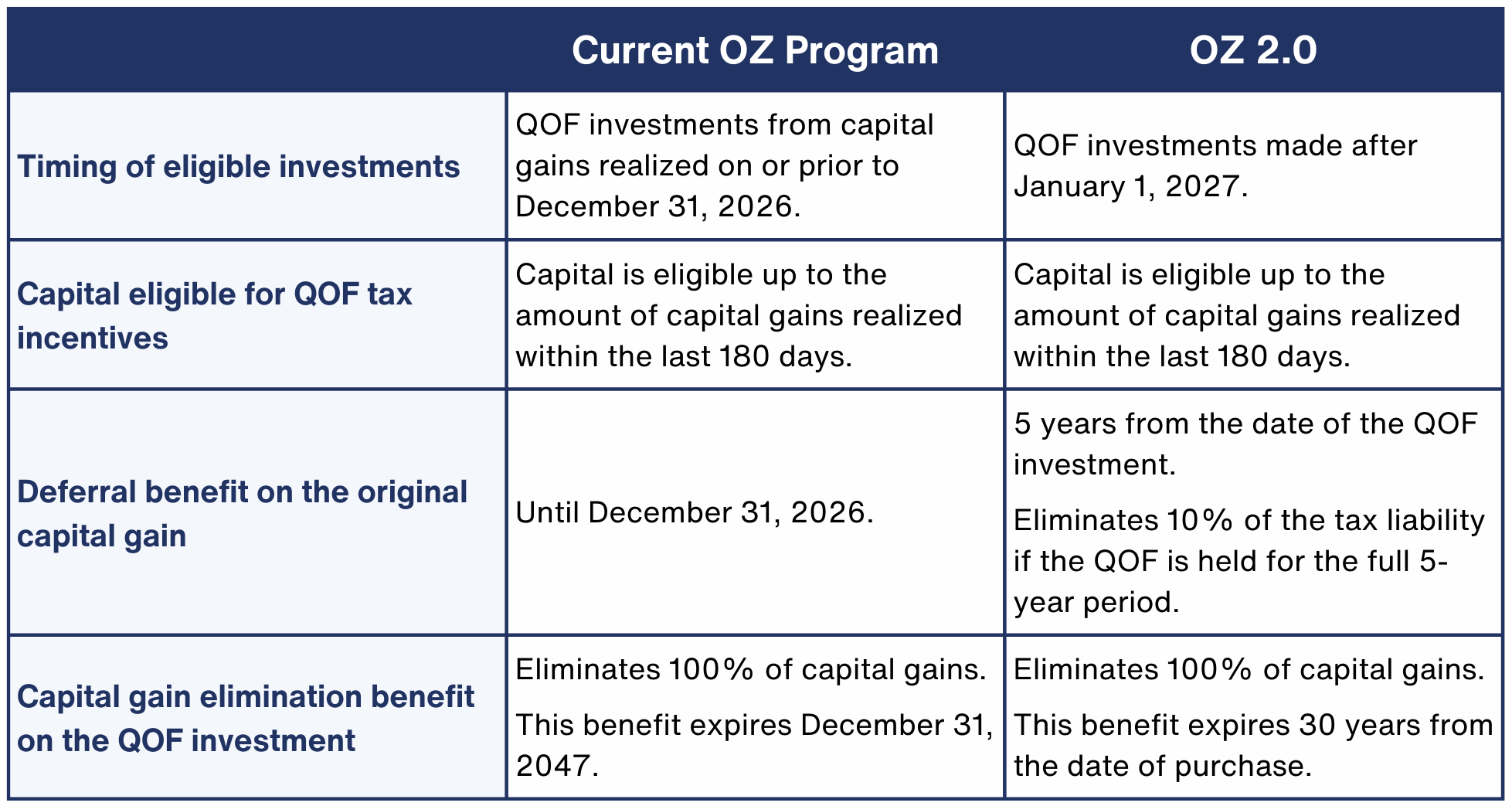

- Investment Timeline: Investors have a capital gains 180 day rule for qualified opportunity fund reinvestment from the date a gain is realized to move capital into a fund.

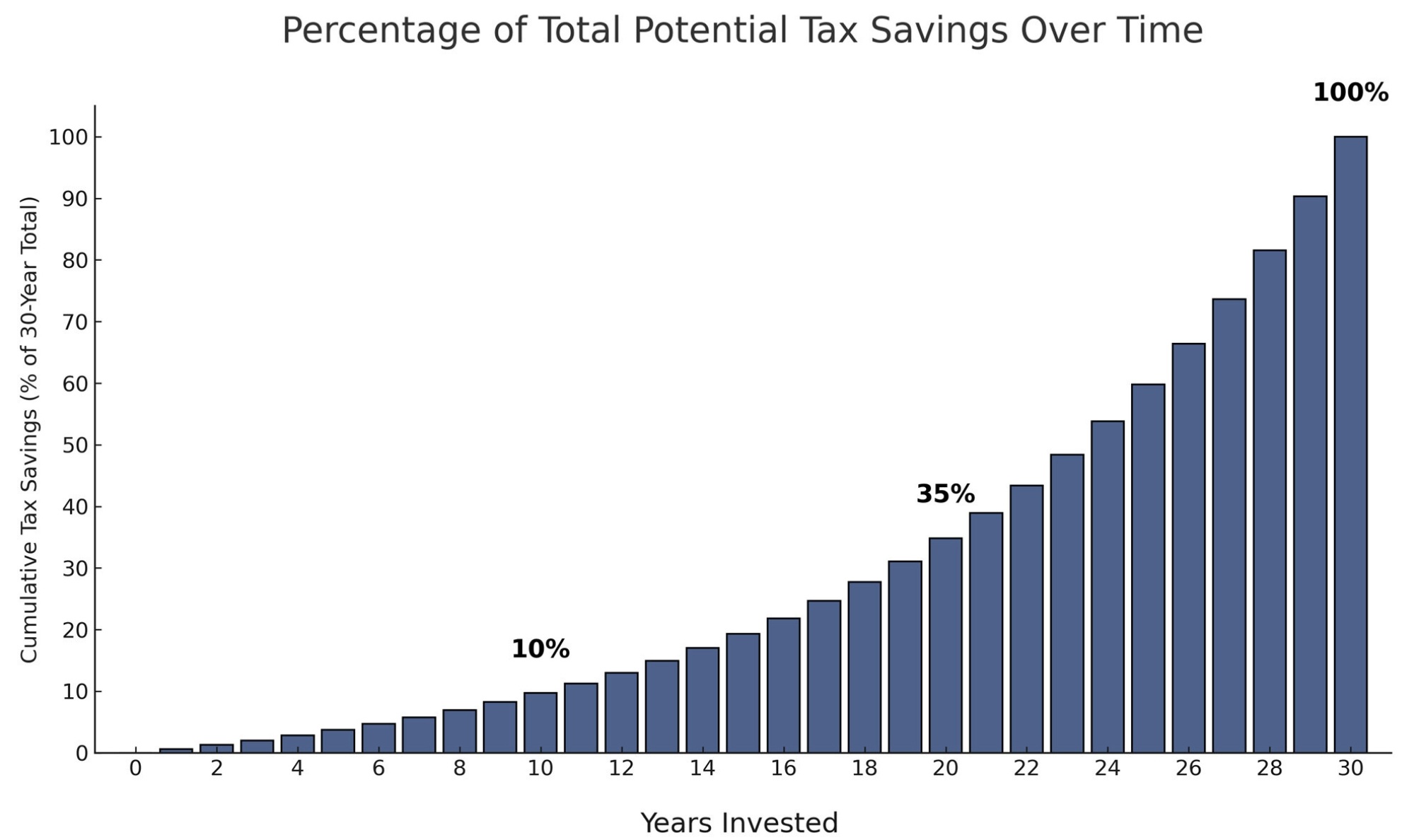

- The 10-Year Milestone: Holding a Qualified Opportunity Fund investment for at least 10 years enables you to eliminate 100% of the capital gains tax on any post-investment appreciation.

- Wealth Longevity: Under the new Opportunity Zone 2.0 framework, tax-free growth status is protected for 30 years, lasting through December 31, 2047.

- Legislative Shift: The One Big Beautiful Bill Act (OBBBA) introduces a 10% basis step-up for new investments and a specialized 30% basis step-up for funds focused on rural revitalization.

- Capital Velocity: From 2018 through 2023, the program has attracted an estimated $150 billion in private equity into distressed communities.

As we approach the critical June 2026 window, savvy investors are looking toward Qualified Opportunity Funds as the ultimate vehicle for capital gains reinvestment. With the One Big Beautiful Bill Act in play, the era of Opportunity Zone 2.0 offers unparalleled wealth preservation strategies—potentially providing 30 years of tax-free growth that exceeds the reach of traditional Roth IRAs.

Uncapped Growth: Roth IRA vs Qualified Opportunity Funds

For high-net-worth individuals, tax-advantaged accounts often feel like a drop in the bucket. While a Roth IRA is arguably the gold standard for tax-free savings, it is hindered by strict annual contribution limits and income phase-outs. Even if you max out your contributions every year, the scale of capital you can shield remains modest. This is where Qualified Opportunity Funds redefine wealth preservation.

A Qualified Opportunity Fund functions like a Roth IRA on a much larger scale, but without the contribution caps. While you might be restricted to a $7,500 annual limit in a Roth IRA, you can reinvest millions in realized capital gains into a QOF. Furthermore, Qualified Opportunity Funds use what is essentially pre-tax capital—gains you have already made but haven't yet paid taxes on—whereas a Roth IRA requires post-tax income.

What this means for you is a dual-layered tax advantage. First, you defer the tax on the initial gain. Second, all future growth within the fund is protected from the 3.8% Net Investment Income Tax and the capital gains tax entirely. For investors who have already exhausted their qualified opportunity funds vs roth ira contribution limits, the QOF serves as a secondary, uncapped strategy to shield large liquidity events from future tax rate increases.

| Feature | Roth IRA | Qualified Opportunity Fund |

|---|---|---|

| Contribution Limit | $7,000 - $8,000 annually | Unlimited (based on realized gains) |

| Income Limits | Yes (Phase-outs apply) | No |

| Source of Funds | Post-tax ordinary income | Reinvested capital gains |

| Tax on Appreciation | 0% | 0% (after 10-year hold) |

| Investment Types | Stocks, bonds, ETFs | Real estate, businesses in QOZs |

The 180-Day Rule and the 2026-2027 Bridge Strategy

Precision is the hallmark of tax planning, and the capital gains 180 day rule for qualified opportunity fund reinvestment is the most critical deadline to manage. Generally, you have 180 days from the date of a sale to move those gains into a fund. However, if your gains are generated through a partnership or S-corporation, your 180-day clock usually starts on December 31st of the year the gain was realized, giving you significantly more breathing room.

We are currently entering a transitional phase often referred to as bridging OZ 1.0 to OZ 2.0 for 2026 investors. Under Internal Revenue Code Section 1400Z-2, the original deferral period is set to trigger a tax event in late 2026. However, the One Big Beautiful Bill Act provides a strategic pivot point. Gains realized after July 10, 2026, are uniquely positioned to bridge into the Opportunity Zone 2.0 tax benefits starting January 1, 2027.

By utilizing this bridge strategy, investors can opt for a rolling five-year deferral period and a 10% basis step-up that was previously phasing out. The impact of one big beautiful bill act on opportunity zone investing cannot be overstated; it effectively resets the clock for a new generation of wealth. For those holding gains from earlier years, reinvesting into new QOFs can help maintain the tax-free status while accessing the updated incentives for longer-term holds.

Timeline: Critical Dates for QOF Investors

- July 10, 2026: The benchmark date for realizing gains that can bridge into the OZ 2.0 framework.

- December 31, 2026: The original tax deferral deadline for OZ 1.0 investments.

- January 1, 2027: Official commencement of the Opportunity Zone 2.0 rolling five-year deferral benefits.

- December 31, 2047: The final date to exit a fund while maintaining 100% tax-free appreciation.

The Rural QOF Advantage: A 30% Basis Step-Up

The OBBBA has pivoted the program’s focus toward areas that need it most, resulting in massive tax benefits of rural qualified opportunity funds under OBBBA. While urban zones continue to see significant interest, rural revitalization has become the new frontier for those seeking the highest mathematical return on tax savings.

In the original program, approximately 8,764 census tracts were designated as zones. The updated OBBBA rules have refined these areas, removing high-income tracts and doubling down on rural locations. For investors who commit to these qualified rural areas, the standard 10% basis step-up is tripled. A 30% basis step-up is available for those who hold their rural QOF investment for a minimum of five years.

This "super-bonus" is designed to create a long-term mechanism for capital to flow into underserved markets. From an investor perspective, a 30% reduction in the deferred tax bill, combined with the 100% elimination of tax on the backend appreciation, makes rural projects some of the most competitive risk-adjusted returns in the market. When evaluating fund managers, look for those with a proven track record in niche rural development, as the compliance requirements for the 90% asset test are often more stringent in these locations.

Compliance and Risks: 1031 Exchanges and State Traps

It is common to compare Qualified Opportunity Funds to the traditional 1031 exchange. While both offer tax deferral, the QOF provides far more flexibility. In a 1031 exchange, you must reinvest both your principal and your gain into "like-kind" property. In a QOF, you only need to reinvest the gain. This allows you to pull your original principal off the table—effectively de-risking your position while still enjoying the growth.

However, compliance is where many investors trip. To maintain tax-advantaged status, a fund must satisfy the 90% asset test, meaning 90% of its holdings must be Qualified Opportunity Zone Business property. If the fund fails this test, it faces monthly penalties, and persistent failure can lead to disqualification, triggering a massive tax bill. Furthermore, investors must be wary of state-level non-conformity. While the federal government offers these benefits, several states do not recognize the tax deferral for state income tax purposes.

State Non-Conformity Checklist If you reside in or earn income from the following states, be aware that you may still owe state capital gains taxes even if your federal tax is deferred:

- California: Does not conform to the federal QOZ program.

- Mississippi: Treats QOF gains as taxable income.

- North Carolina: Does not recognize the tax-free appreciation on the exit.

- Pennsylvania: Generally does not follow the federal deferral rules.

- New York: Has specific decoupling rules that may affect certain resident investors.

Selecting qualified opportunity fund exit strategies after 10 year hold is just as important as the entry. Because you have until 2047 to exit, you have the luxury of time to wait for the ideal market window. This 30-year runway is a powerful tool for generation-skipping wealth or funding a lengthy retirement without the drag of the net investment income tax.

FAQ

What is a Qualified Opportunity Fund and how does it work?

A Qualified Opportunity Fund is an investment vehicle organized as a corporation or partnership for the purpose of investing in Qualified Opportunity Zone property. It works by taking realized capital gains and deploying them into businesses or real estate within specific census tracts. By doing so, the investor can defer their original tax bill and grow the new investment tax-free.

What tax benefits do Qualified Opportunity Funds offer?

The program offers three primary benefits: tax deferral on original gains until late 2026 (or longer under OBBBA), a cost basis adjustment that reduces the amount of original tax owed, and a 100% basis step-up on the new investment. This final benefit effectively eliminates all capital gains tax on the appreciation of the fund investment if held for 10 years or more.

How long must you hold a Qualified Opportunity Fund investment?

To receive the maximum benefit—the 100% elimination of tax on new growth—you must hold the investment for at least 10 years. Shorter hold periods of five or seven years may qualify you for a smaller cost basis adjustment on your original deferred gain, but the "tax-free" exit only triggers after the tenth anniversary of the investment.

What are the deadlines for investing capital gains into an Opportunity Fund?

Typically, you must invest your gains within 180 days of the sale that generated the gain. For individuals receiving a Schedule K-1 from a partnership, the 180-day window usually starts at the end of the partnership’s tax year (December 31). Missing these windows can result in a loss of eligibility for the tax benefits of the program.

How does a Qualified Opportunity Fund differ from a 1031 exchange?

A 1031 exchange requires you to reinvest the entire proceeds of a sale (principal plus profit) into a similar real estate asset. A Qualified Opportunity Fund only requires you to reinvest the profit. Additionally, QOFs allow for investments in businesses and equipment, not just "like-kind" real estate, and they offer a total tax exemption on future growth, which 1031 exchanges do not.

The window for the most aggressive Opportunity Zone 2.0 benefits is opening soon. If you are sitting on substantial gains from stock sales, business exits, or real estate, mastering the timing of these funds is the difference between a standard return and a legacy-defining wealth event. Planning now for the 2026-2027 transition ensures your capital remains productive, protected, and private for decades to come.