Quick Facts

- Target Goal: $1 million net worth by age 35.

- Required Savings Rate: 30% to 50% of post-tax income.

- Core Strategy: Disciplined budgeting combined with systematic index fund investing.

- Key Benchmark: Portfolio fees should remain below 0.20% to avoid erosion.

- Age-Based Target: Aim for 1x to 1.5x annual salary in savings by age 35.

- Tax Advantage: Maximize 2026 SALT deductions and SECURE 2.0 contributions.

- Asset Protection: Use a revocable living trust early to avoid probate and manage estate growth.

Reaching a seven-figure net worth early requires more than just a high salary; it demands a disciplined financial independence roadmap. One banking professional achieved his $1M goal by 35 by mastering specific wealth building strategies. By focusing on asset allocation and maximizing tax-advantaged accounts, he outperformed the average trajectory. This guide breaks down his net worth growth tips and how 2026 legislation like the SECURE Act 2.0 can accelerate your own journey.

The Banking Pro’s Blueprint: Staying the Course to $1M

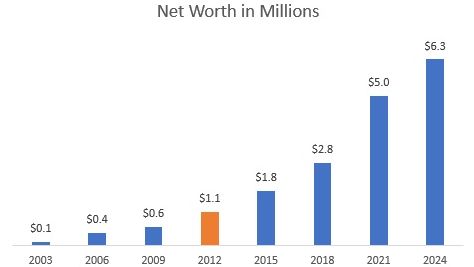

In the world of personal finance planning, we often see a stark contrast between high earners and high net worth individuals. While many young professionals in high-paying sectors enjoy a lifestyle of luxury, few manage to convert those earnings into a lasting foundation of wealth before the standard retirement age. The reality of the American landscape is telling: the median net worth for Americans under age 35 is approximately $39,000, whereas the average person who reaches a $1 million net worth in the United States does not do so until age 61. Breaking into the seven-figure club by your mid-thirties requires a radical departure from the norm.

The banking professional featured in this case study followed a path that was less about picking the next hot stock and more about staying the course during market volatility. By age 35, he had successfully accumulated a $1 million net worth through a relentless focus on high savings rates, often between 30% and 50% of his post-tax income. This trajectory highlights that reaching $1M by 35 is possible only through heavy lifting in the early years. It requires leaning into frugal living early on to let compound interest do the heavy lifting later. For those building wealth on 200k salary or similar high-income paths, the challenge isn't the capacity to save, but the discipline to do so when your peers are upgrading their lifestyles.

Achieving this milestone starts with understanding the order of operations. The core answer to building massive wealth involves maximizing every available tax-advantaged tool while maintaining a standard of living that remains far below your means. It is about closing the gap between what you earn and what you spend, then funneling that gap into assets that provide consistent capital appreciation.

Disciplined Budgeting: The ‘Core vs. Optional’ Framework

The primary tool used by this banking professional wasn't a complex proprietary software, but a simple habit of tracking expenses with excel for net worth management. He utilized a "Core vs. Optional" framework, which distinguishes between the non-negotiables of life and the variables that can be trimmed. By categorizing spending this way, he treated his budget like a corporate balance sheet.

Core expenses include housing, utilities, basic groceries, and insurance. Optional expenses include dining out, high-end travel, and premium subscriptions. To maintain a high savings rate, he followed a few strict rules:

- The 12-Year Car Rule: Keeping a reliable vehicle for over a decade to avoid the cycle of car payments.

- Rent Optimization: Avoiding the move to a "luxury" apartment even when income doubled.

- Automated Savings: Setting up direct transfers to brokerage accounts on payday so the money was never "seen" as disposable.

Financial institutions like T. Rowe Price suggest that by age 35, you should have saved between 1 and 1.5 times their current annual salary. For high earners in the financial sector, like an investment banking associate, maintaining an aggressive posture can lead to having between $500,000 and $600,000 in savings by age 30.

Preventing lifestyle inflation for high earners is perhaps the most difficult emotional hurdle. As colleagues purchase second homes or luxury watches, the banking pro remained focused on his personal balance sheet. He viewed every $1,000 saved not as a sacrificed luxury, but as a building block for his financial independence roadmap. When you implement disciplined budgeting methods, you are essentially buying back your future time.

The 2026 Investment Stack: Maximizing Returns and Accounts

Investing for 2026 requires a nuanced understanding of new legislation and changing tax limits. The banking professional’s investment strategy was built on a tiered hierarchy. He focused on index fund investing with low expense ratios, ensuring that portfolio management fees remained below 0.20% to prevent the erosion of long-term gains.

In the 2026 environment, maximizing retirement and health savings accounts means staying abreast of the SECURE Act 2.0. This legislation has significantly altered the landscape, particularly with "super" catch-up contributions that allow those nearing mid-career to accelerate their savings. Furthermore, the 2026 landscape introduces government incentives for child savings 2026, often colloquially referred to as "Trump Accounts," which allow for early childhood education and long-term savings with specific tax benefits.

His investment "stack" followed this specific order:

- Employer Match: 100% contribution to the 401(k) match limit.

- HSA Maximization: Utilizing the Health Savings Account as a "stealth" IRA for triple tax advantages.

- Roth or Backdoor Roth IRA: Prioritizing after-tax growth while income limits allowed.

- Maximum 401(k) Contributions: Utilizing the increased limits set by the SECURE Act 2.0.

- Taxable Brokerage: Directing all remaining surplus into diversified index funds.

By employing dividend reinvestment across all these accounts, he ensured that every cent of profit was immediately put back to work. This systematic approach meant he didn't have to time the market; he simply had to be in the market. Over time, the asset allocation shifted slightly as the portfolio grew, balancing aggressive growth funds with stable value assets to protect the principal.

Long-Term Protection: Safeguarding Your Success

Once you cross the mid-six-figure threshold, wealth building strategies must shift from pure accumulation to asset protection. For the banking professional, reaching the $1 million mark was a trigger to look at estate planning essentials. It is not enough to hit the number; you must protect it from taxes, probate, and liability.

A key move was the creation of a revocable living trust. This legal tool ensures that assets are managed seamlessly in the event of incapacitation and avoid the expensive, public process of probate. For high earners, protecting net worth growth tips often involve shielding your legacy from excessive state and federal taxes. With the federal estate tax exclusion limits fluctuating, having a trust in place provides a flexible framework to adapt to changing laws.

Moreover, insurance is treated as a strategic asset class rather than just an expense. High-limit umbrella insurance policies protect the $1M net worth from personal liability claims, while term life insurance provides a safety net for any dependents without the high costs of whole-life policies. Safeguarding your success means ensuring that a single legal or medical event cannot wipe out a decade of disciplined saving and index fund investing.

As you approach your goal, your focus should move toward capital appreciation that is tax-efficient. This might involve holding assets for more than a year to trigger long-term capital gains rates or utilizing tax-loss harvesting during market dips. The banking pro’s journey shows that hitting the million-dollar milestone is the result of many small, correct decisions compounded over a decade of dedication to a financial independence roadmap.

FAQ

What is the fastest way to build wealth?

The fastest way to build wealth is to maximize the gap between your income and expenses and invest that surplus immediately into broad-market index funds. Increasing your primary income while maintaining a stagnant standard of living allows for an exponentially higher savings rate. Utilizing tax-advantaged accounts like 401(k)s and HSAs ensures that more of your money stays working for you rather than going to the government.

What habits do most self-made millionaires have in common?

Self-made millionaires typically share a commitment to long-term thinking and frugality. They tend to avoid status symbols, drive older cars, and live in modest homes relative to their income. Most importantly, they track their finances meticulously—often using tools like Excel—and treat their personal savings as a non-negotiable monthly "bill" that must be paid before any discretionary spending occurs.

What are the safest long-term wealth building strategies?

Diversified index fund investing is widely considered one of the safest long-term strategies. By owning a small piece of hundreds or thousands of companies, you mitigate the risk of any single company failing. Combined with dollar-cost averaging, where you invest a set amount regardless of market conditions, you lower the risk of entering the market at a peak. Staying the course during market volatility is essential to capture the full benefits of compound interest.

What are the primary pillars of financial independence?

The primary pillars include a high savings rate, debt elimination, automated investing, and tax optimization. First, you must eliminate high-interest debt that erodes your net worth. Second, you must establish a system where a significant percentage of your income is automatically invested. Finally, you must use legal vehicles like 401(k)s, IRAs, and trusts to protect your wealth from taxes and legal liabilities.

How long does it typically take to build significant wealth?

For the average person, building a $1 million net worth takes about 30 to 40 years of consistent saving and investing. However, for those who can maintain a savings rate of 40% or higher, this timeline can be compressed into 10 to 15 years. The length of time is determined less by the total amount of money you make and more by the percentage of that income you are able to keep and invest.